Listen to the article

Listen to the article

Saving money is a common practice for fulfilling short-term financial requirements. Anything from seven days to less than twelve months can be considered a short-term investment, even if there isn’t a set time frame for them.

Several options are available when it comes to short-term investing products. Here are five short-term investment options compared based on taxation, tenure, returns, and liquidity.

Best Investment plans for 1 Year Short-Term Investment Options

| Investment Options | Returns | Yield | Security | Volatility Risk | Tax Implications |

| Fixed Deposits | 3-8% | 12-20% | Bank Guarantee | Low | Interest income is taxable |

| Real estate structured debt | 12-18% | Varies | Secured by Real Estate | Low-None | None |

| Post office time deposits | 6.9% | Varies | Sovereign Guarantee | Low | Interest income taxable |

| Recurring Deposits | 4-8% | Varies | Bank Guarantee | Moderate to high | Subject to taxation based on your income slab |

| Debt mutual funds | 6-9% | Varies | Diversified Portfolio | High | Taxation on gains |

Bank fixed deposits

One of the safest investment choices that Indians prefer is fixed deposits. One benefit is that you can start FDs straight from your bank account, which makes it easier to store extra money for short periods of time.

Tenure: Fixed Deposits (FDs) are available with varying durations, spanning from as short as 7 days or 14 days to up to a decade. The specific durations may differ from bank to bank. It is possible to renew FDs upon maturity and reinvest the funds. Under the rules of the Deposit Insurance and Credit Guarantee Corporation (DICGC), each depositor in a bank is insured for a maximum amount of Rs 5 lakh, covering both the principal and interest.

Liquidity: Certain banks may offer FDs without the option for premature withdrawals. To avoid locking funds for a single duration, investors have the option to divide their investments across different maturity periods using a technique called ‘laddering.’

Returns: Depending on the individual’s requirements, FDs offer various interest payout options, such as monthly, quarterly, half-yearly, or yearly, as well as cumulative interest. The interest rates banks offer are influenced by factors like the Reserve Bank of India’s (RBI) repo rate and the bank’s own funding costs. For instance, as of September 5, 2023, State Bank of India (SBI) provides interest rates ranging from 3% to 5.75% for FDs with tenures between 7 days and 1 year, while HDFC Bank offers rates between 3% and 6%.

Taxation: The interest earned from FDs is considered a part of one’s income and is subject to taxation based on the applicable income slab. If the total interest earned across all bank branches exceeds Rs 10,000 in a given year, the bank deducts Tax Deducted at Source (TDS) on the interest amount.

Real Estate Structured Debt

In India, one of the best short-term investment choices is real estate structured debt. This option offers fixed-income opportunities supported by collateralized real estate. It is one of the best options for short-term investments in India, with a strong chance of yielding large returns.

Tenure: Investors with a minimum investment horizon of 36 months may invest through alternative investing platforms like Assetmonk.

Liquidity: Compared to certain other investment options, structured debt backed by real estate may be less liquid because it could take time to sell or withdraw from these investments.

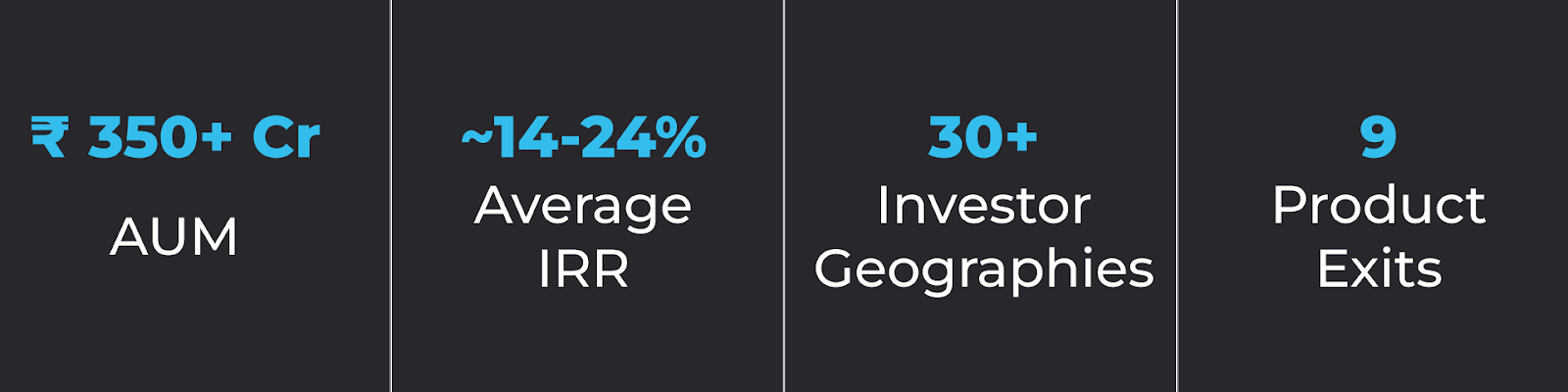

Returns: Real estate-backed structured debt has the potential to yield substantial returns through capital growth or interest payments. You can earn an impressive 12-18% internal rate of return (IRR) through structured debt.

Rental yields from real estate investments also offer the possibility of a consistent revenue stream. Investors can profit from consistent income flows due to the rising demand for rental properties, particularly in desirable areas and cities with high rental demand.

Taxation: Subject to relevant laws and regulations, real estate investments in India may provide tax advantages such as house loan deductions, rental income exemptions, and capital gains tax advantages on long-term investments.

Post office time deposits

Post office time deposits are savings schemes offered by the post office. Individuals can deposit their money for fixed periods, ranging from one year to five years, and earn a specified interest rate on their savings. The government backs these deposits and provides a secure way for people to save money and earn interest over time.

Tenure: The Post Office also offers time deposits similar to bank Fixed Deposits (FDs). These deposits, known as Term Deposits (TDs), can be made for 1, 2, 3, or 5 years.

Liquidity: As per the information on the India Post website, no premature withdrawals can be made within the first six months of depositing the amount. If the TD account is closed after 6 months but before 1 year, the interest rate applicable will be equivalent to the Post Office Savings Account Interest rate. Interest is paid annually, and no additional interest is provided on any interest amount that remains due but has not been withdrawn by the account holder.

Returns: For short-term investment, one can consider a 1-year Post Office Time Deposit (POTD), where the interest is paid annually but calculated quarterly. The government evaluates and adjusts the rates every quarter. As of the quarter ending September 30, 2023, the 1-year POTD offers an interest rate of 6.9%.

Taxation: The interest earned on these deposits is considered a part of the individual’s income and is subject to taxation based on their income slab.

Recurring Deposits

To save regularly for the short term, for example, 6, 9, or 12 months, one can opt for a bank Recurring Deposit (RD). In an RD, the individual has to make regular deposits at fixed intervals for a specific duration and will receive the lump sum amount upon maturity. Most banks allow investing in RDs online.

These deposits allow you to accumulate a lump sum over time and earn interest on their savings.

Tenure: The minimum deposit period is six months, while the maximum is ten years.

Liquidity: Premature withdrawals are not allowed. However, some banks may permit you to close your account before maturity under specific circumstances.

Returns: The interest rate is fixed at the start of the tenure and remains unchanged until maturity. Upon maturity, one will receive a lump sum amount, including the regular investments and the interest earned. The interest rate offered on RDs is consistent with that of a Fixed Deposit.

Taxation: The interest earned on RDs is considered a part of the individual’s income and is taxed as per their income slab. If the interest income exceeds Rs 10,000 a year (including interest on bank deposits) across all branches of the bank, Tax Deducted at Source (TDS) will be applied.

Debt mutual funds

Investment vehicles known as debt mutual funds combine the capital of several participants to buy a variety of debt securities. The primary investments made by these funds are in fixed-income securities, which include corporate and government bonds, treasury bills, money market instruments, and other debt instruments.

Debt mutual funds come in different categories, such as liquid, short-term, income, and gilt, each with its own risk-return profile.

According to the most recent data, investors who want a consistent income stream with comparatively less risk than equity investments are still drawn to debt mutual funds. These funds are expertly managed by seasoned fund managers who evaluate market conditions, credit quality, and interest rate trends to make well-informed investment choices.

Tenure: To take advantage of long-term capital gain provisions, holding these investments for a minimum of three years is recommended. Furthermore, if withdrawals from most debt funds are made before 36 months, exit load fees may apply.

Liquidity: Because of their liquidity, investors can purchase or sell fund units on any given business day. Because of this aspect, they are a desirable alternative for people looking for flexibility and simple access to their invested funds.

Returns: Regular interest payments and possible capital gains of the underlying debt securities are two ways that investors can profit. Interest rate changes and the portfolio’s credit quality have an impact on returns.

Taxation: For the first three years of ownership, investors in debt funds are liable to income tax on capital gains based on their income tax band. They are then subject to taxes at a rate of 10 percent in the absence of indexation or 20 percent with indexation advantage.

Bottom Line

Preserving capital while potentially earning interest is the primary goal of any chosen short-term investment. For example, it’s crucial to prioritise the safest options—high-yield savings accounts, term deposits, and liquid funds—when setting up an emergency fund. Despite the liquidity benefits, emergency funds should never be allocated to equities stocks, commodities, or derivatives.

As one of India’s best alternative investing platforms, Assetmonk stands out for offering a wide variety of attractive solutions to discerning investors. These opportunities allow people to explore the world of structured debt investments in the commercial real estate industry as well as a carefully selected array of alternative investment options.

FAQs

1. What are the Best Investment plans for 1 Year

A. Some of the Best Investment plans for 1 Year include fixed deposits, Treasury bills, liquid mutual funds, and short-term bond funds…etc

2. How do I choose the right short-term investment option for less than one year?

A. When choosing a short-term investment option, consider factors such as the desired level of risk, expected returns, liquidity, and the investment duration. It’s essential to assess your financial goals and individual risk tolerance before deciding.

3. Are these short-term investment options suitable for beginners?

A. Yes, these short-term investment options are suitable for beginners due to their lower risk profile and shorter investment duration. They provide a relatively stable and secure way to grow your funds over a shorter time frame.

4. Are short-term investments plans for 1 Year are Safe?

A. Short-term investments generally carry lower risk compared to long-term investments. However, the level of safety may vary depending on the specific investment option chosen. It is important to review the risk factors associated with each investment and make an informed decision.